Dollar-Cost Averaging versus Lump-Sum Investing: What Sophisticated Investors Actually Do

When it comes to long-term investing, one of the most common pieces of advice is to use Dollar-Cost Averaging (DCA). Many financial advisors recommend it as a disciplined way to invest over time. But an important question remains: Is dollar-cost averaging actually the best strategy for a sophisticated long-term investor?

To answer this, it helps to look at both the mathematics of investing and the behavior of professional fund managers who manage billions of dollars.

What Is Dollar-Cost Averaging?

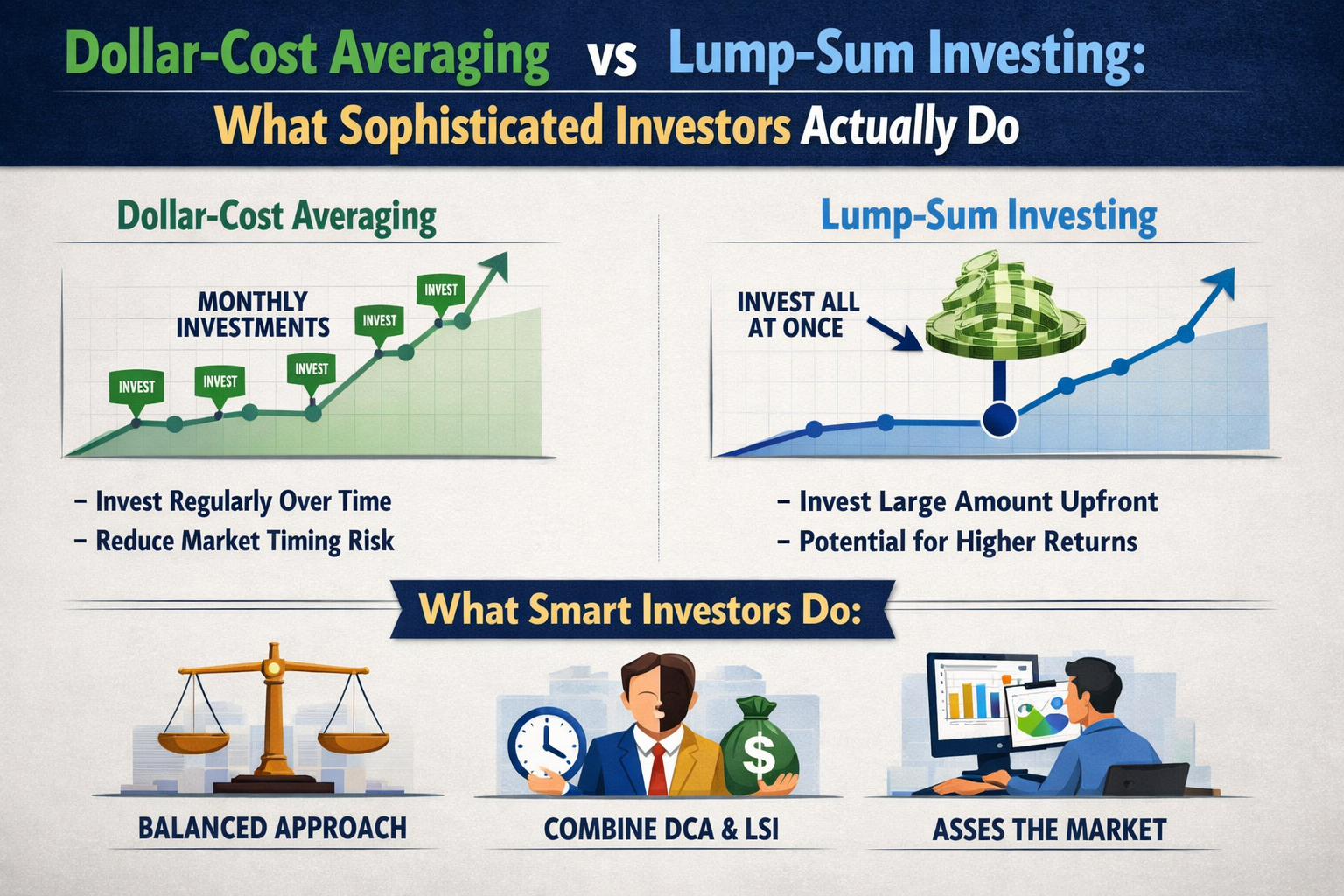

Dollar-cost averaging is a strategy where an investor divides a lump sum of money into smaller portions and invests those portions at regular intervals such as monthly or quarterly, regardless of market conditions.

The idea is simple:

By investing gradually, you reduce the risk of investing all your money right before a market downturn.

When prices are high, you buy fewer shares.

When prices are low, you buy more shares.

Over time, this averages out your cost per share.

The Case for Lump-Sum Investing

While DCA is widely recommended, academic research consistently shows that lump-sum investing often produces higher expected returns over long periods. This is because stock markets historically trend upward over time. When investors delay investing their capital, some of that money remains in cash rather than participating in market growth.

In other words: Time in the market generally beats timing the market.

If you already have money available to invest, putting it to work sooner allows it to benefit from compounding earlier. This doesn’t mean lump-sum investing always wins in the short term. If markets drop immediately after investing, DCA would have produced a better outcome. But over longer time horizons, the upward trend of markets tends to favor investing sooner rather than later.

What Do Professional Investors Do?

Interestingly, most professional fund managers and institutional investors do not rely on mechanical dollar-cost averaging. Instead, they typically deploy capital when they believe opportunities exist.

For example:

- Hedge funds often build positions based on valuation or market conditions.

- Value investors may buy larger positions when they believe an asset is significantly undervalued.

- Quantitative funds allocate capital according to statistical signals and risk models rather than fixed schedules.

Sometimes professionals scale into positions gradually, but this is usually done for tactical reasons; such as managing risk or avoiding market impact when buying very large amounts of shares. It is not the same as traditional dollar-cost averaging.

Why Dollar-Cost Averaging Became Popular

If lump-sum investing often performs better mathematically, why is DCA so widely recommended?

The answer lies in investor psychology! DCA helps solve several behavioral challenges:

- Reduces regret risk: investing a large amount right before a market decline can feel painful. DCA spreads out that risk.

- Encourages discipline: regular investing helps people stay consistent instead of waiting for the “perfect” moment.

- Matches real-world cash flow: most individuals earn income gradually through salaries, so they naturally invest gradually as well.

Because of these benefits, DCA remains a useful tool for many investors especially those who prioritize emotional comfort and consistency.

A Simple Example

Imagine an investor has $120,000 available to invest.

Scenario 1: Lump-Sum Investing

The investor puts the entire $120,000 into the market today.

If the market grows at an average annual rate of 7%, the investment would grow to approximately $236,000 after 10 years.

Scenario 2: Dollar-Cost Averaging

Instead, the investor invests $10,000 per month for 12 months.

During that first year, some of the money remains in cash instead of participating in market growth. As a result, the portfolio may end up slightly smaller over the long run compared to investing everything immediately.

However, if the market declines during that first year, the DCA strategy may have purchased shares at lower prices and could temporarily outperform the lump-sum approach.

This example highlights the key trade-off:

- Lump sum offers higher expected returns

- DCA offers smoother entry and reduced timing risk

A Strategy Many Sophisticated Investors Use

Rather than choosing strictly between the two approaches, many experienced investors use a hybrid strategy.

For example:

- Invest 60–80% of available capital immediately

- Keep 20–40% in reserve to invest if markets decline or new opportunities emerge

This approach captures most of the benefit of being invested early while still allowing flexibility if markets become more attractive later.

The Most Important Factor: Time

Regardless of the entry strategy, the most important determinant of long-term investment success is time spent in the market.

Short-term timing differences tend to matter far less than:

- maintaining consistent exposure to quality assets

- staying invested through market cycles

- allowing compounding to work over many years

Even investors who entered markets at imperfect times historically have still benefited significantly from long-term market growth.

Concluding Remarks

Dollar-cost averaging is a valuable strategy for building investing discipline and reducing psychological stress. For many individuals, it remains a practical approach.

However, when capital is already available to invest, historical evidence suggests that investing sooner rather than later often leads to better long-term results. Professional investors rarely rely on strict DCA schedules. Instead, they focus on valuation, opportunity, and maintaining long-term exposure to the market.

Ultimately, the best strategy is the one that keeps investors consistently invested, disciplined, and focused on the long term.

Sources: Vanguard Research, FinanceWonk, Yahoo Finance, and Bloomberg.